Typically, an employee of company A, who is moonlighting for company B, would be on the payrolls of both. However, it is quite possible that he or she may just do a stray one-off project for some firms.

Tax implications are explained via scenarios:

Scenario 1 |

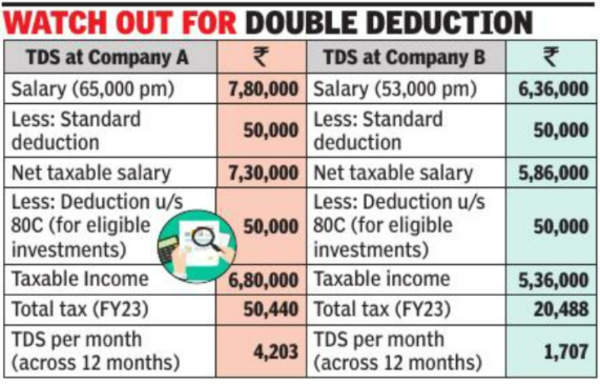

Sudhakar G (name is illustrative) is a full-time employee of company A. He is a technical writer for company A and is working from Bengaluru for a Singapore-based client of his employer. The time difference means the client doesn’t hassle him during evenings. Thus, working for company B during night shift on a US-centric project fits perfectly with plans of earning a second income.He is on the payrolls of both the companies. Neither know he is employed with the other. Here is what would happen from the tax perspective.

Both companies would take into consideration the standard deduction of Rs 50,000. It should be noted that this deduction is limited to Rs 50,000 in a year. Further, both companies could factor in the tax benefit-related investment declarations, if so made by Sudhakar, for computing the tax deducted at source (TDS).

In short, it would translate to reduced TDS. Sudhakar needs to ensure tax obligations are met via regular advance tax payments (see table).

Sudhakar has not opted for the concessional tax regime, but is taking advantage of the normal tax slabs with tax deductions. His taxable salary for fiscal 2022-23 is Rs 13,66,000 (after deducting Rs 50,000), against which the 80C deduction is Rs 50,000, making his taxable income Rs 13,16,000. Against this, the tax liability works out to Rs 2,15,592.

Hot tip |

Puneet Gupta, partner, people advisory services at EY India, says, “Individuals may be able to moonlight if their employers do not impose restrictions. Income tax law permits an individual employed simultaneously with more than one employer to submit details of salary from one employer to the other in Form 12B. Such other employer will then consider total salary while deducting tax at source, avoiding TDS shortfall.”In Sudhakar’s case, to meet the TDS shortfall of Rs 1,44,664 owing to double deduction of tax benefits by both employers, Sudhakar will need to pay advance tax on a quarterly basis. Else, there will be penal interest. Advance tax norms require that 15% of the tax liability for the year must be paid by June 15, 45% by September 15, 75% by December 15 and 100% by March 15.

If Sudhakar is a consultant for company B, the following illustration will apply to him too:

Scenario 2 |

For Ramesh N (name is illustrative) his foray into moonlighting began when he helped an entrepreneur-friend with some web designing over weekends. Soon, he got many such projects. His income for fiscal 2022-23 from such projects is estimated at Rs 12,50,000.Such income will be taxed under the head ‘Income from business or profession’. Ramesh can claim depreciation against capital expenditure such as laptop purchased for doing these projects. He can also claim routine expenses, such as stationery, travel and data charges. As his income exceeds Rs 2.5 lakh, he will be required to maintain books of accounts. However, this can be forgone if the presumptive tax mechanism is opted for, where 50% of the gross moonlighting income is treated as taxable income. If Ramesh opts for presumptive taxation scheme, he would be liable to pay whole amount of advance tax on or before March 15. If the presumptive taxation scheme is not opted for, advance tax will be payable each quarter.

Hot tip |

“Where the individual is earning professional income in addition to salary, income tax law also permits the employee to report details of other income to the employer, which can be considered while deducting TDS. This may avoid hassles for the individual to deposit quarterly advance tax,” says Gupta.

!(function(f, b, e, v, n, t, s) {

window.TimesApps = window.TimesApps || {};

const { TimesApps } = window;

TimesApps.loadFBEvents = function() {

(function(f, b, e, v, n, t, s) {

if (f.fbq) return;

n = f.fbq = function() {

n.callMethod ? n.callMethod(…arguments) : n.queue.push(arguments);

};

if (!f._fbq) f._fbq = n;

n.push = n;

n.loaded = !0;

n.version = ‘2.0’;

n.queue = [];

t = b.createElement(e);

t.async = !0;

t.src = v;

s = b.getElementsByTagName(e)[0];

s.parentNode.insertBefore(t, s);

})(f, b, e, v, n, t, s);

fbq(‘init’, ‘593671331875494’);

fbq(‘track’, ‘PageView’);

};

})(

window,

document,

‘script’,

‘https://connect.facebook.net/en_US/fbevents.js’,

);if(typeof window !== ‘undefined’) {

window.TimesApps = window.TimesApps || {};

const { TimesApps } = window;

TimesApps.loadScriptsOnceAdsReady = () => {

var scripts = [

‘https://static.clmbtech.com/ad/commons/js/2658/toi/colombia_v2.js’ ,

‘https://www.googletagmanager.com/gtag/js?id=AW-877820074’,

‘https://imasdk.googleapis.com/js/sdkloader/ima3.js’,

‘https://tvid.in/sdk/loader.js’,

‘https://timesofindia.indiatimes.com/video_comscore_api/version-3.cms’,

‘https://timesofindia.indiatimes.com/grxpushnotification_js/minify-1,version-1.cms’,

‘https://connect.facebook.net/en_US/sdk.js#version=v10.0&xfbml=true’,

‘https://timesofindia.indiatimes.com/locateservice_js/minify-1,version-14.cms’

];

scripts.forEach(function(url) {

let script = document.createElement(‘script’);

script.type=”text/javascript”;

if(!false && !false && !false && url.indexOf(‘colombia_v2’)!== -1){

script.src = url;

} else if (!false && !false && !false && url.indexOf(‘sdkloader’)!== -1) {

script.src = url;

} else if (!false && !false && (url.indexOf(‘tvid.in/sdk’) !== -1 || url.indexOf(‘connect.facebook.net’) !== -1 || url.indexOf(‘locateservice_js’) !== -1 )) {

script.src = url;

} else if (url.indexOf(‘colombia_v2’)== -1 && url.indexOf(‘sdkloader’)== -1 && url.indexOf(‘tvid.in/sdk’)== -1 && url.indexOf(‘connect.facebook.net’) == -1){

script.src = url;

}

script.async = true;

document.body.appendChild(script);

});

}

}

More News

Paytm shares drop 5% following resignation of COO Bhavesh Gupta | India Business News – Times of India

Lok Sabha elections phase 3: Banks are closed on May 7 in these cities – check list | India Business News – Times of India

Planning to invest in NPS? Top 5 reasons you should consider National Pension System – Times of India